Economic Benefits of NSW Gov Public EV Fast Charging Strategy

The NSW Government analyzed the cost-benefit of public fast-charging infrastructure for electric vehicles (EVs), comparing funded and unfunded scenarios over 20 years. Results indicated that

The Future of Data Centre Electrical Grid Impacts

The rapid expansion of data centres to support AI, cloud computing, and digitization is reshaping electricity demand and challenging grid planning. Energeia’s research highlights the

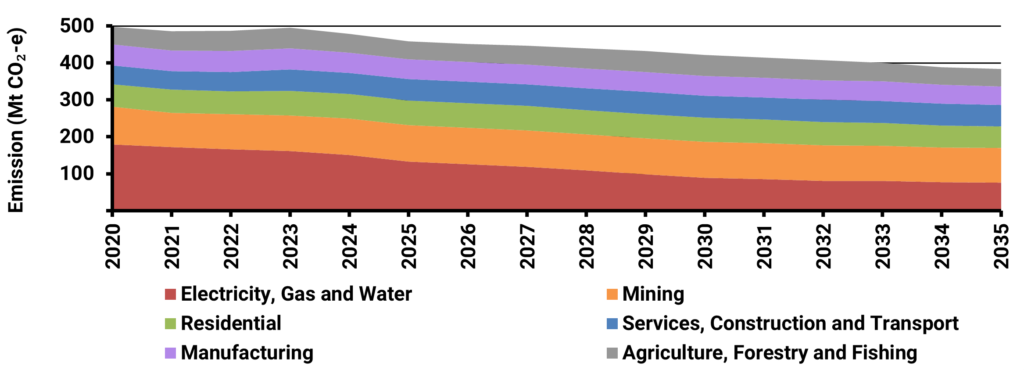

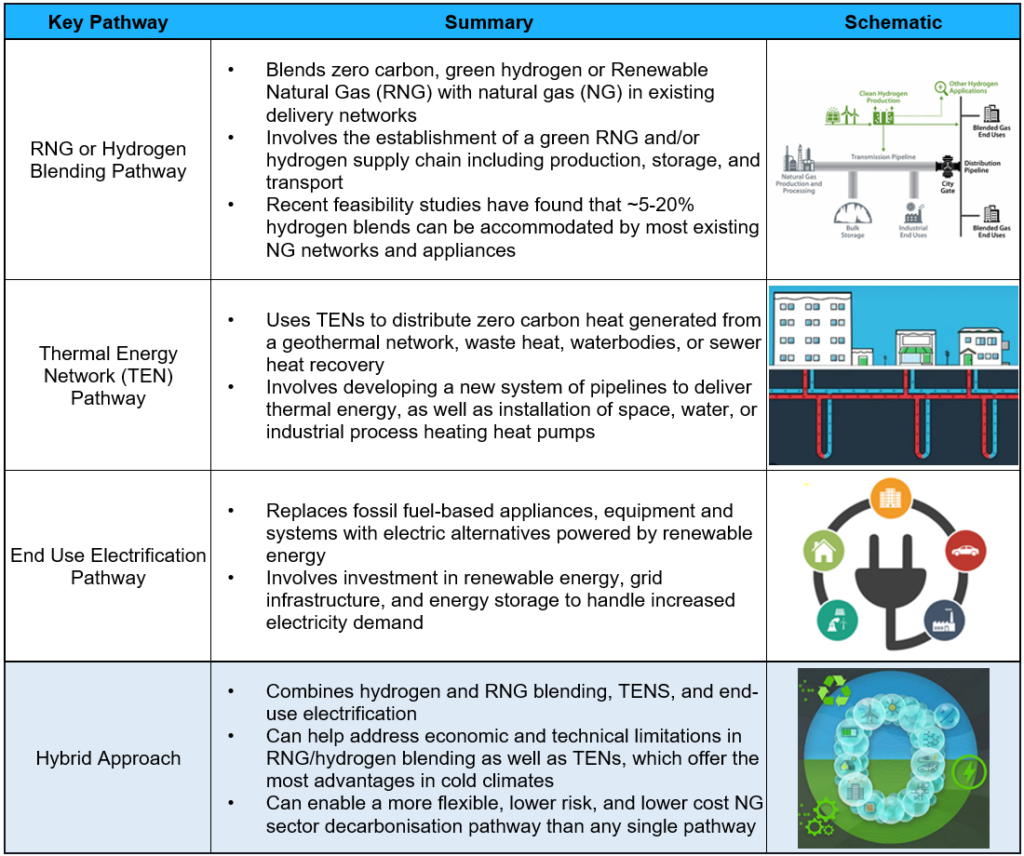

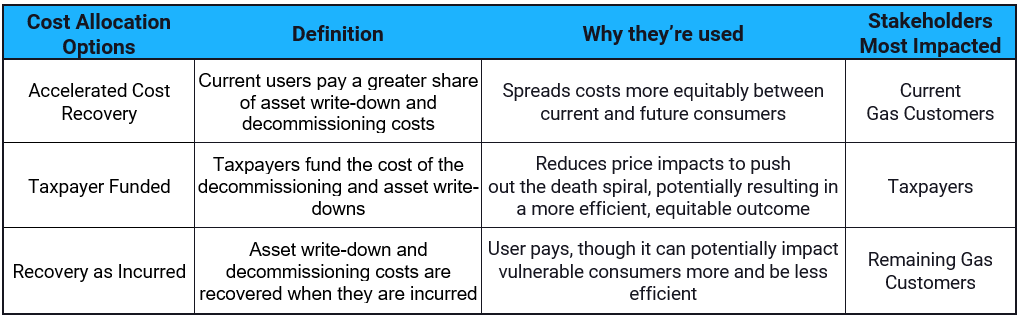

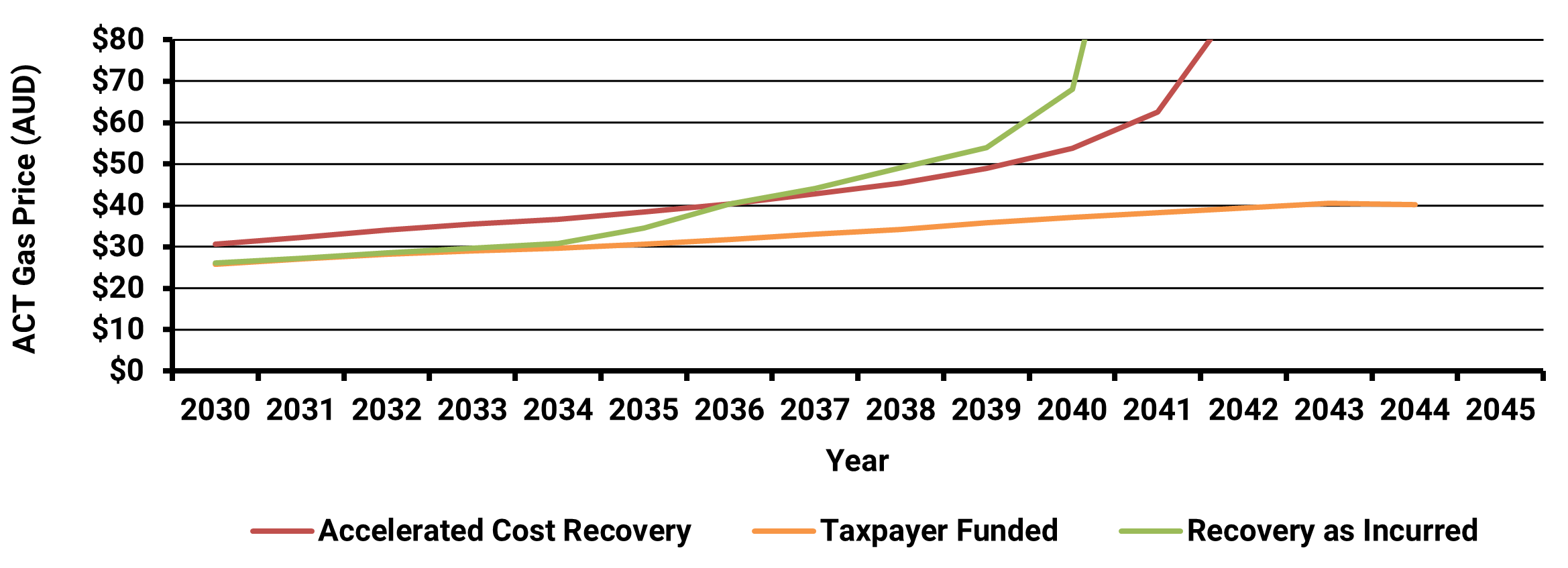

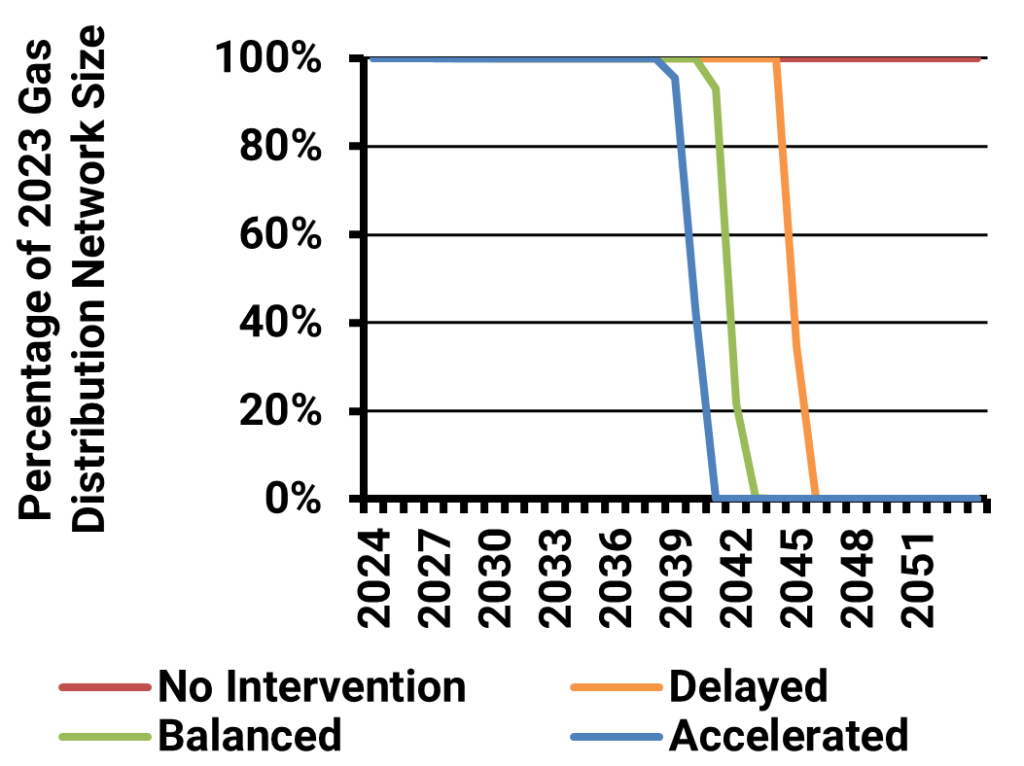

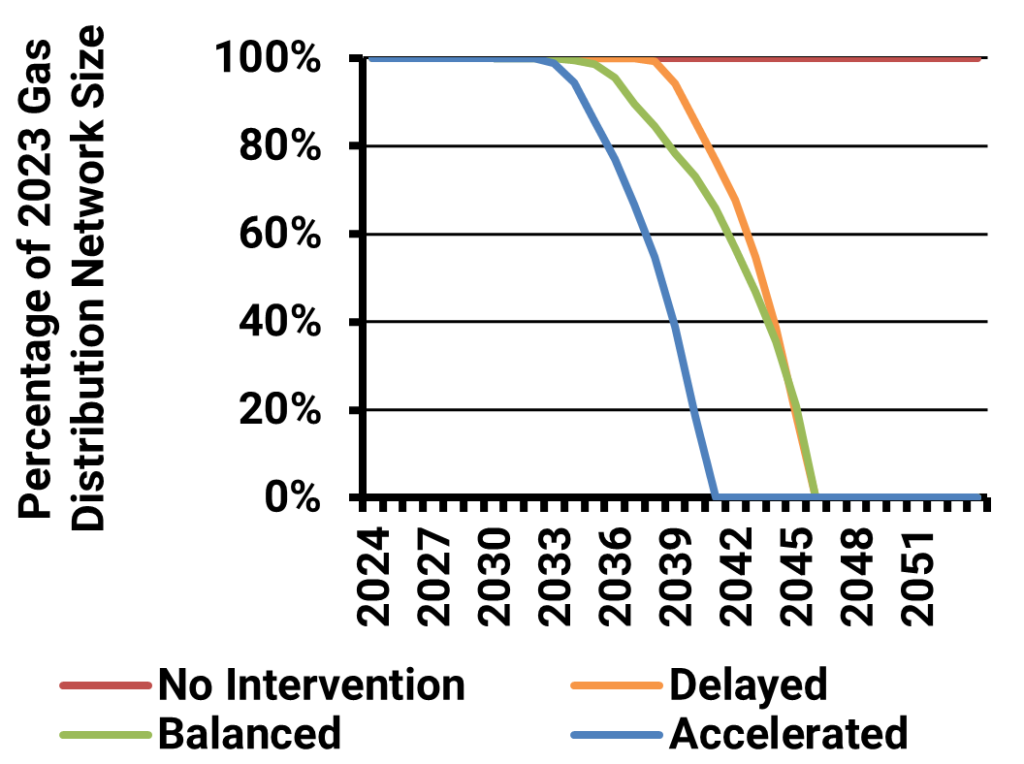

Natural Gas Decarbonisation Strategies and Impacts

Energeia’s research outlines key pathways, including renewable gas blending, thermal energy networks, and end-use electrification, all vital for achieving carbon targets while minimizing economic disruption.